April Investor Guide

Inside this month's Issue:

Articles

Preventing Stupid Economic Tricks

The policies that undermind productivity growth

April Investor Guide

Preventing Stupid Economic Tricks

The policies that undermind productivity growth

Restarting the global growth engine obviously involves doing a lot of the right things in order to enhance productivity. But the other side of the equation involves avoiding policies that undermine productivity growth.

Restarting the global growth engine obviously involves doing a lot of the right things in order to enhance productivity. But the other side of the equation involves avoiding policies that undermine productivity growth.

The current transition has been slowed by the entrenched economic interests of the mass-production era, which have tried desperately to prevent disruption. That's only natural.

However, the sophisticated mechanisms brought to bear during the transitional phase of the Mass Production Revolution and the Digital Revolution dwarf those available at a comparable point in the three preceding Techno-Economic Revolutions.

Therefore, the dislocations of the Great Depression as well as the Great Recession, which really started with the bursting of the "tech bubble," have been extended and softened. In the process, politicians have taken a short-term view, putting in place policies that shield their constituents from the pain caused by economic "evolutionary pressure." Those constituents are multifaceted, ranging from bondholders to tort lawyers to labor unions to tax lawyers to the perennial underclass to auto dealers and taxi drivers. The list of "oxen being gored" seems endless.

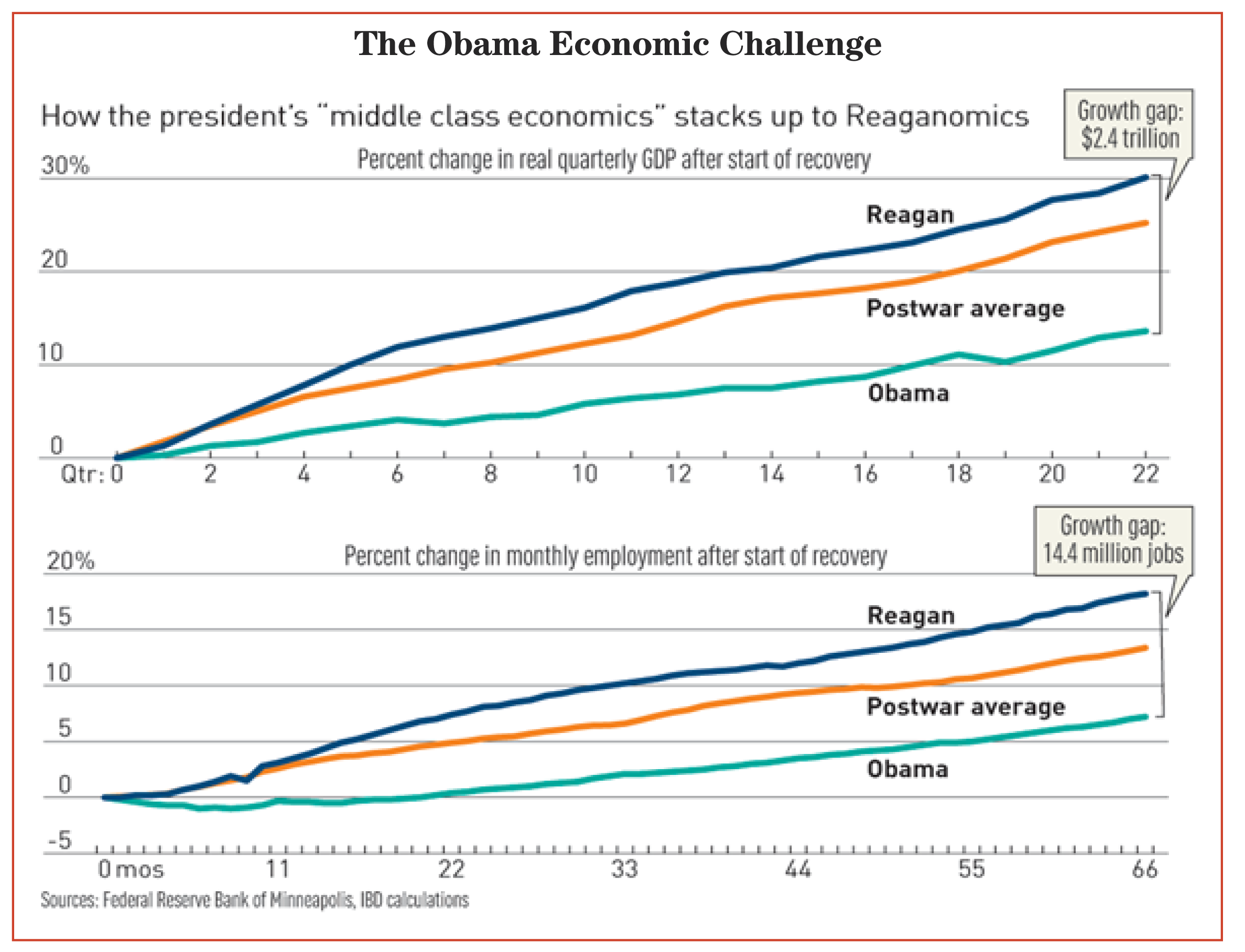

The Obama Economic Challenge

Given that nobody likes the discomfort of short-term radical change, even when the long-term benefits from that change are obvious, it's unrealistic to expect this behavior to disappear. The challenge is to learn from the consequences of our actions.

That's what is unique about this juncture in history. The Digital Revolution itself has given us, for the first time ever, the data and tools needed for a thorough forensic analysis of our economic decisions.

Percent Distribution of US Households

Moreover, the fragmentation and transparency associated with the Digital Revolution have enabled us to conduct a serious, "evidence-based" debate in a way that would have been impossible during the Railroad Revolution or the Mass Production Revolution. The New Deal, the Great Society, and even the Reagan Revolution were based on a set of "theoretical constructs" that made logical sense, but had not been thoroughly tested in a way that enabled us to separate the noise from the signal.

Today, we have a unique opportunity to make policy decisions based increasingly on empirical evidence, where differences of opinion are based on "values" but we all share a common understanding of cause-and-effect. It's like the discovery of Newtonian mechanics; the laws are the same whether applied to building an orphanage or a concentration camp; only the values and objectives differ.

Consider the implications: The values and visions of socialists and Ayn Rand-style libertarians still clash, but we now have evidence to show what works. Soviet Russia and North Korea proved that an economy devoid of market mechanisms (such as prices, consumers, and capital markets) was not viable, long-term. On the contrary, Singapore has proven that a laissez-faire economy can deliver a high and rapidly rising standard of living for many.This helps narrow the policy options that can be considered.

The immediate upshot is that decision makers now have the tools required to avoid what the Strategic Wealth Advisor editors call Stupid Economist Tricks. These are policies put in place with limited validation because they are consistent with a widely accepted, but largely untested, economic ideology. As we are increasingly able to evaluate decisions based on objective evidence, the debate will now shift to competing "values." That will not only create a more honest discussion, but one that leads to fewer "unintended consequences."

Given this trend, we offer the following forecasts for your consideration:

First, by 2025, "cost-benefit analysis" will lead to a major rollback of the $2 trillion per year U.S. regulatory compliance burden. A harbinger of this trend is "The Regulations from the Executive in Need of Scrutiny Act" introduced by Sen. Rand Paul. It would force Congress to approve or deny every rule proposed by the executive branch with an economic impact of $100 million or more. In 2014, the executive branch finalized 200 such rules. So-called "sunset" legislation has also been proposed that would require Congress to regularly re-authorize regulations; otherwise they would simply be deactivated. In the past, an unambiguous cost-benefit analysis was impossible, but today big data analytics make such timely analysis by the GAO and CBO quite realistic. Permanent rules promulgated by bureaucrats were appropriate for the Mass Production era and before, but they make little sense in the Digital era.

Second, as soon as 2017, dynamic scoring will become the new touchstone for U.S. legislative programs, leading to much more realistic assessments of the impact that legislation will have on our economic well-being. As much as 55 percent of experts recently surveyed by the University of Chicago business school agreed that ". . . official forecasts provided to Congress would be more accurate if the CBO and JCT tried to estimate fully how the proposed tax changes would affect growth ... ," while only 25 percent disagreed. Although this position has traditionally been held mostly by conservative economists, better data and models have made dynamic scoring increasingly acceptable across the political spectrum; the White House recently applied this methodology in building its economic case for new immigration policies announced in November. Larger data sets and better analytic tools will shrink the error bars on these forecasts to ever more manageable levels.

Third, over the coming decade, big data will shift the education debate toward 'what's good for students and society, in the long-run.' In a data-poor world, administrators and teachers' unions armed with anecdotal evidence had a huge advantage. But increasingly, we all are starting to have access to real-world experimental data on the costs and outcomes of education alternatives; and these data are frequently at odds with the status quo. Parents, students, taxpayers, legislators, and employers can all look at this empirical evidence and determine how best to invest a finite pool of resources.

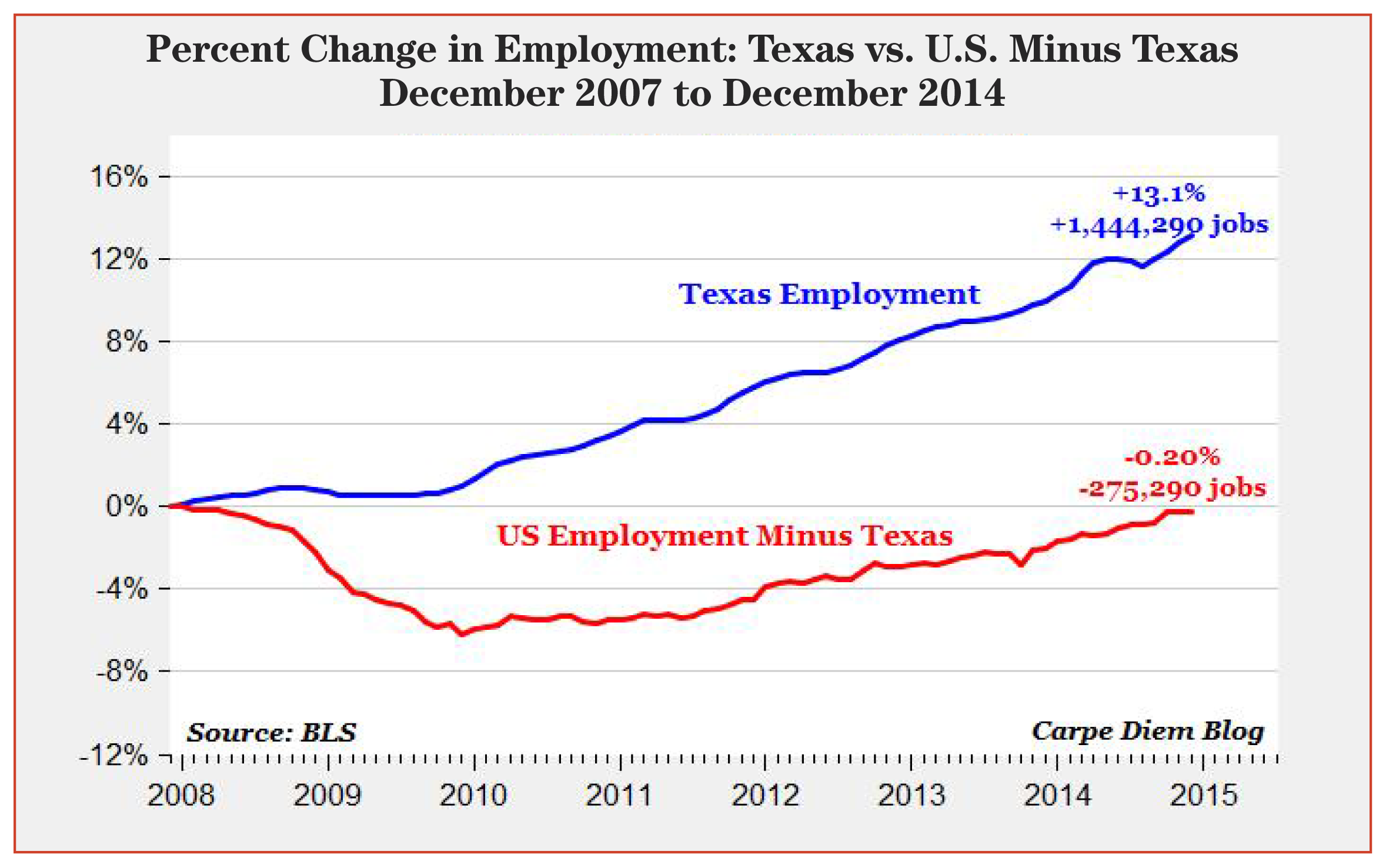

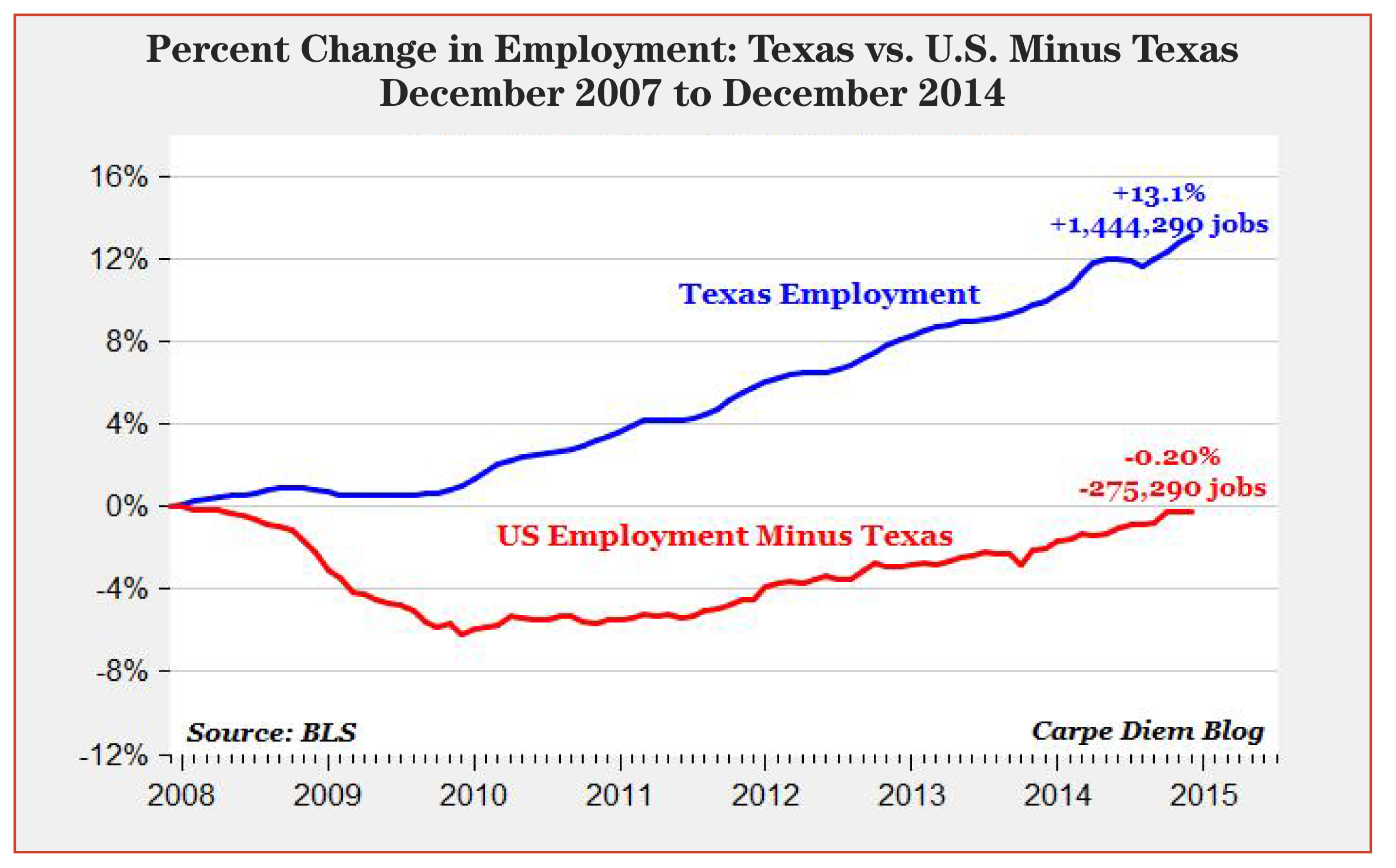

Percent Change in Employment

This is already happening at the college level in states as diverse as South Carolina, Wisconsin, Georgia, and Ohio. Within the next five years, this resource re-allocation will take center-stage in the K-12 sector.

Data will finally empower a "school choice revolution," where vouchers will be used to fund everything ranging from traditional public schools, to private campus-based schools, to online home school programs. Similarly, realistic models of human capital and employment opportunities may finally put to rest the fantasy of "college for all" and replace it with a system focused on building high-ROI vocational skills.

Fourth, issues of income and wealth inequality will not go away, but the current "class-warfare dynamic" will evaporate as the problem and its solutions become better understood. The one size-fits-all education paradigm has contributed to the "skills gap," which has hollowed out the American middle class. Recent research shows that the middle class has largely disappeared because many have moved up into the growing "affluent class," while low-income Americans have not moved up into the middle class.4 This is largely due to the disappearance of traditional mid-skilled jobs and our failure to prepare people for a new set of middle skilled jobs. Similar shifts have occurred in every

Techno-Economic Revolution, dating back to the original 18th century Industrial Revolution. Rather than redistributing wealth, as advocated by the worshippers of what we call "the Flying Piketty Monster," the growing mountain of evidence will confirm that it's wiser to redistribute productive capabilities in the form of knowledge and skills. This new quantification of the underlying problems will also lead to a redesign of the social safety net so as to reinforce, rather than undermine, family values and personal happiness.

Fifth, granular models and "what-if" analyses will help prevent ill-conceived regulations enacted mostly for political expediency, like mark-to-market accounting, Dodd-Frank, and Sarbanes-Oxley. No clearer example exists of why we need to avoid the unintended consequences of rules, regulations, and policies than the imposition of mark-to-market accounting rules prior to the collapse of the housing bubble in 2008. Fundamentally, the housing bubble was not unlike the S&L bubble of nearly 20 years earlier. As Peter Wallison of AEI makes clear in his book Hidden in Plain Sight,the securitized mortgages called collateralized mortgage obligations (CMOs) were held by a wide range of institutions, which then issued credit default swaps and other derivatives backed by those securities. When the housing collapse eliminated much of the collateral value in the homes, markets in the CMOs froze and firms were forced under mark-to market rules to value the CMOs at "zero." This, in turn, triggered the collapse of the derivatives market, creating a global panic. That panic only subsided once mark-to-market rules were suspended in March 2009. Had the regulators thoroughly modeled scenarios, it's doubtful that mark-to-market rules would have been promulgated and that the financial panic of 2008 would have occurred.

Sixth, hard data will increasingly redefine the battle between neo-Keynesian and supply-side economic policymakers. For many years, a war has raged between those who believe economic vitality can be assured through demand-oriented transfer payments and those who believe growth is best. encouraged by supply-side investments in innovation and production capacity.

Since government has no money of its own, if it happiness. chooses to stimulate demand by giving money to people or buying things, it has to either borrow or tax resources from the private sector. And that means the private sector has less to invest in productive activity.

While the Strategic Wealth Advisor editors are relatively confident that the supply-side view will be confirmed as more data become available, it's always possible that the Keynesian view could prevail. Regardless of where the data comes out, it will be much better to base such crucial decisions on solid empirical evidence rather than the "divinations of economic oracles."

Seventh, fact-based policy decisions will be possible as we use evidence from economic experiments at the state and local levels to determine the efficacy of various alternatives.

Consider the possibilities:

Do these unnatural monopolies make sense in the 21st century? We'll find out. By laying bare the economic realities, discussions that have been obscured by assumptions and biases will finally be argued in quantifiable terms.