January Investor Guide

Inside this month's Issue:

Articles

The Great Investment Opportunity of 2015

January Investor Guide

The Great Investment Opportunity of 2015

I’m pleased to report that the Strategic Wealth Advisor strategies closed out 2014 with a gain of 16.37%. That’s a 20% greater gain than enjoyed by those who invested in the S&P 500. And we didn’t use margins, options, or penny stocks.

I’m pleased to report that the Strategic Wealth Advisor strategies closed out 2014 with a gain of 16.37%. That’s a 20% greater gain than enjoyed by those who invested in the S&P 500. And we didn’t use margins, options, or penny stocks.

This means we’re still among the less than 2% of investors and funds that have beat the S&P 500 total return for over 5 consecutive years.

Most important, our 5-year and 10-year track records continue to beat the Dow, S&P 500, and even Warren Buffett’s Berkshire Hathaway by sizeable margins.

So what’s ahead for the markets and for Strategic Wealth Advisor in 2015?

The biggest single story is likely to be in the energy sector. This month’s issue includes our much anticipated Special Report, “The Great Oil Opportunity of 2015.” Not only do we foresee major opportunities for investors as “cheap energy stocks” outperform, but we see the drop in energy prices as a catalyst finally unleashing the Deployment Phase of the Fifth Techno-Economic Revolution.

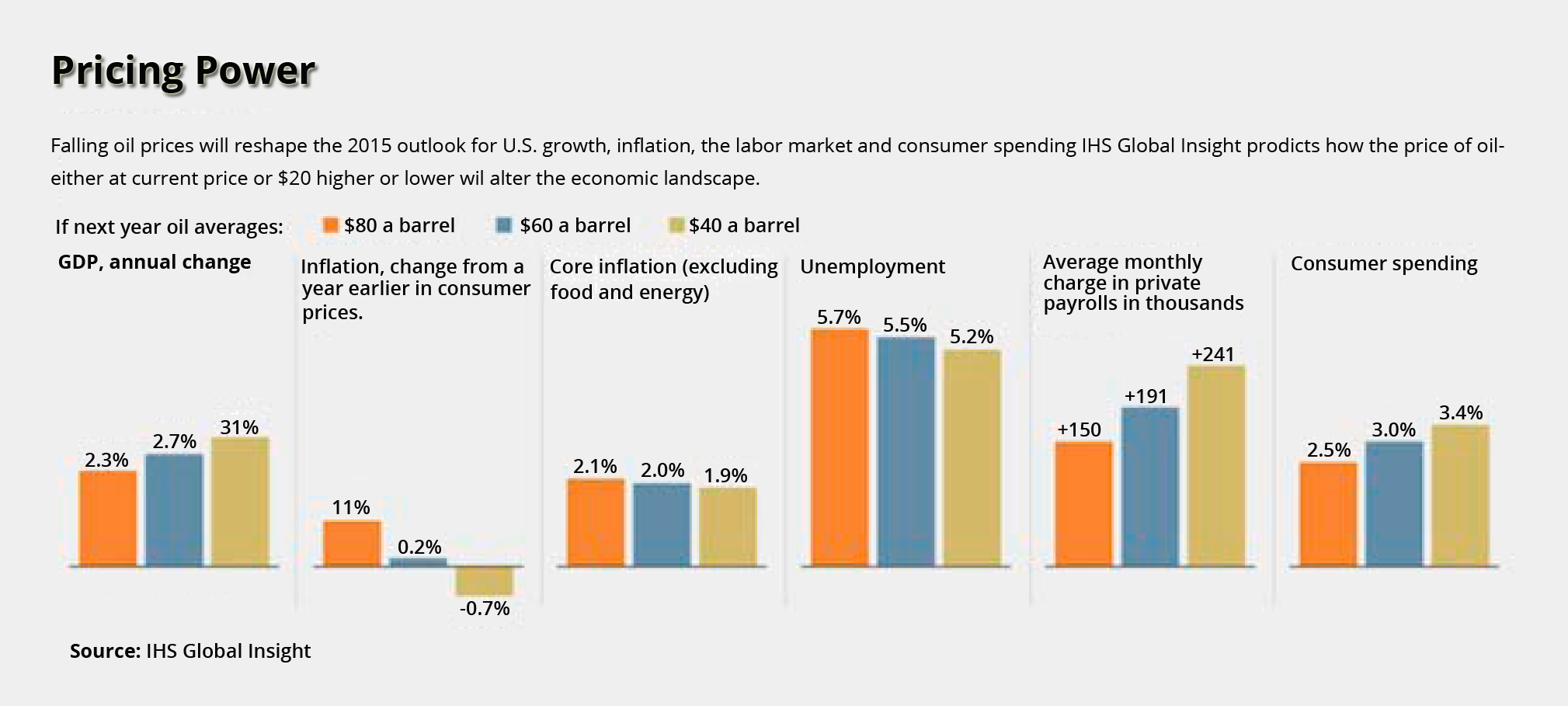

The implications for the broader economy in 2015 are very positive, as summarized in the chart below from IHS Global Insight. GDP growth & consumer spending will accelerate, unemployment will shrink, payrolls will expand, and the trade deficit will shrink. Outside the OECD, energy-intensive economies like China, Vietnam, and India will reap huge benefits from the annual $1.3 to $2.0 trillion income transfer we’ll see from oil exporters to oil importers. If anything, the IHS forecasts for the U. S. are too conservative.

Chart A

Ignore the “gloom and doom merchants” like Harry Dent, who claim that collapsing oil prices foreshadow another financial disaster. Just as the disruption of any industry by a new technology has a wide range of consequences, the current shift will produce winner and losers. However, the net impact of lower oil prices on the global economy, and the U. S. in particular, will be unambiguously positive.

Also, ignore the green energy pundits whining about “stranded assets.” As Chris Knittel, a professor of energy economics at the Massachusetts Institute of Technology put it, "Low gas prices can undo progress we've made in green technology. People are less likely to adopt more fuel-efficient vehicles, and companies have less incentive to invest in new technologies." Bottom line: the “climate change train” is off the rails and it’s not likely to be leaving the station in the coming decade. In fact, the 18-year “warming hiatus” coupled with 5+ years of $60 to $70 per barrel oil pretty much ensures that the business case for green energy (i. e., wind, water, solar) is dead on arrival. By the time these technologies are ready for prime-time various nuclear and GMO-based bio-fuel technologies will make them non-starters.

The biggest threat to financial stability is probably Russia, which has an enormous debt load denominated in appreciating U. S. dollars. Worse yet, the oil and gas revenue needed to service that debt continue to plummet. Fortunately, most other highly leveraged countries are net energy importers who will benefit from lower prices.

Because we’re bullish on the broader economy as well as the energy sector, the Strategic Wealth Advisor team is buying a set of cheap energy stocks that could realistically appreciate 30% to 60% in the 12 months after oil prices bottom. The big challenge is to identify roughly when that bottom has occurred. Obviously, we don’t have to buy in at exactly “the bottom” to reap big rewards. However, it’s smart to get in after the big plunge is over, but before a major recovery has already occurred. Our Special Report addresses the possible scenarios and indicates why we believe January 2015 may be a good time to buy “cheap” the “cheap” large-cap energy stocks we’ve identified.

The North American Energy Revolution has unfolded because of the ability of U. S. energy producers have to produce oil and gas from shale formations at ever-lower cost. A few years ago these cost were very high compared to conventional oil. Drillers in the Eagle Ford, Bakken, and Marcellus formations are now able to produce some of the cheapest natural gas in the world and deliver it to the world’s largest domestic market. Meanwhile, oil from the Eagle Ford formation is already very competitive with most global oil sources outside the Persian Gulf. Other U. S. fields, including the Bakken, are not far behind. So, don’t expect a wholesale collapse in U. S. production and exploration. We’re experiencing a paradigm shift every bit as significant at the rise of OPEC, 40+ years ago.

Expect some aggressive M&A activity in the Energy Sector as companies make acquisitions at bargain basement prices. In 2014, energy was the hottest M&A sector and it’s likely to remain so in 2015. Today these are a huge mountain of junk bond debt issued by small, highly leveraged shale oil and gas firms. The current “crisis” creates an extraordinary opportunity for the major integrated energy companies to acquire valuable asset of these “distressed companies” at bargain-basement prices.